NHS England (“NHSE”) published updated guidance for assuring NHS transactions (“the Guidance”) on 11 October 2022, almost a year after it was consulted on. The previous version of the Guidance was 5 years old and has now been refreshed to reflect learning from past transactions and the evolving NHS landscape.

For the first time, the Guidance has been issued in separate parts under an overall heading of “Assuring and Supporting Complex Change” for each of the various types of NHS transactions which are subject to NHSE’s scrutiny:

- Statutory transactions - mergers, acquisitions, Foundation Trust dissolutions and

- Certain significant service contracts - contracts which expose a Trust or system to significant incremental risk, for instance, where there is material change to the scale or scope of the Trust’s activity.

- Commercial transfers - material sale and purchase agreements short of a whole entity

- Forming or changing a subsidiary - subsidiaries and corporate JVs being formed or materially changed. No changes were made to the existing 2018 guidance meaning that all such transactions remain This part of the Guidance will be updated later in 2022.

- Novel, contentious and repercussive financial arrangements - all such arrangements are reportable. Capital proposals are not within scope; they are assured under a separate approvals process.

- Service reconfiguration - this part of the Guidance comprises the existing NHSE guidance titled “Planning, assuring and delivering service change for patients”.

In our November 2021 article, we summarised the changes which were being consulted on. In this article, we set out the key statutory changes and the regulatory changes which have been adopted (and the ones which haven’t).

Changes to the statutory framework

In the time since the Guidance was consulted on, the Health and Care Act 2022 was passed meaning that ICBs, with system-wide remit, were established as legal entities in their own right. The 2022 Act also resulted in NHS Improvement (comprising Monitor and TDA) being dissolved with their legal powers over statutory NHS transactions being transferred to NHSE. At the same time, amendments were made to the legal processes for statutory transactions. There is now:

- a role for the Secretary of State in all statutory transactions;

- a new power for NHSE to move property and liabilities from one Trust to another, short of a whole entity transfer;

- a practical way to dissolve a Foundation Trust with legal certainty; and a new power for NHSE to dissolve an NHS Trust.

Importantly, the 2022 Act also removed the Competition and Markets Authority’s (“CMA’s”) powers to review mergers of Foundation Trusts. The patient benefit case in a proposed merger will continue to be assessed by NHSE and has now been put forward as the central test - see below. CMA retains jurisdiction over mergers between independent providers and NHS bodies.

Changes to the focus of NHSE’s review process

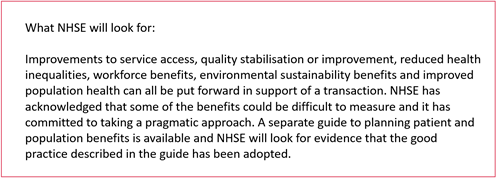

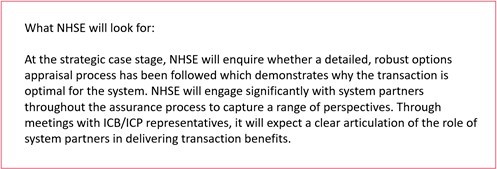

NHSE will now apply an overall test as to whether the deliverable benefits of a transaction materially outweigh the costs and risks. The benefits to patients and the population are defined widely in the Guidance and are broader than direct benefits to patient outcomes. For transactions classed as ‘significant’, benefits will be assessed at both stages of the review process, at strategic case and then at full business case stage, and must be underpinned by detailed plans.

In recognition of the role of ICBs and the wider system, the Guidance introduces an expectation that Trusts and system partners will work together constructively when developing transaction proposals. System support for a proposed transaction will be a key consideration in NHSE’s review process.

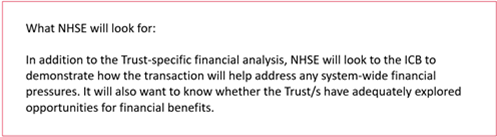

The financial assessment will now test whether the financial benefits of the transaction outweigh the costs over the medium term, without material short-term deterioration.

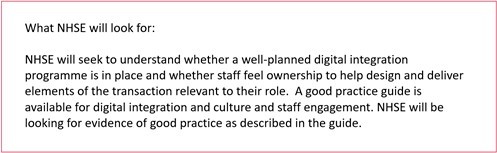

When looking at integration delivery, NHSE has introduced a greater focus on critical success measures such as culture, staff engagement, digital integration and readiness for transformational change.

Other changes

In an effort to reduce regulatory burden and cost, routine external accountants’ opinions are no longer required.

For significant service contracts, novel financing and commercial transfers, NHSE will issue a narrative outcome rather than a red/amber/green rating.

Capital proposals from Foundation Trusts deemed not to be in financial distress have been taken out of the scope of the Guidance. All capital proposals will therefore be assured under NHSE’s capital approvals process.

Assurance of collaboration arrangements

NHSE initially proposed that certain risky, strategic collaborative arrangements should be defined and reviewed as transactions. However, following consultation, NHSE revised its approach and did not issue specific guidance for collaboration reviews. NHSE will instead work closely with systems and providers in order to identify areas of risk and opportunities for shared learning. For more complex arrangements, it may work alongside systems and providers to provide support and feedback.

Next steps

Where Trusts have already started a transaction assurance process under the previous guidance, NHSE will consider transitional arrangements on a case-by-case basis and will support Trusts to transfer to the new Guidance where applicable.